If you’re active duty military (or married to someone who is), you might have heard about premium credit card annual fee waivers — but there’s a lot of confusion out there about what’s law, what’s bank policy, and how it actually works.

This guide will break it all down — the laws, the banks that waive fees, common mistakes, and how to troubleshoot if your fee isn’t being waived.

Step 1: What the Law Actually Says

Before diving into which banks waive annual fees, let’s look at the two key laws that apply to military credit card benefits:

The Servicemembers Civil Relief Act (SCRA)

Think of SCRA as a “pre-service protection.”

Who it protects: Service members who had financial obligations before entering active duty.

What it does: Caps interest rates at 6% and provides other protections like foreclosure relief.

The Military Lending Act (MLA)

MLA is more of a “while-on-active-duty” protection.

Important: This protection only applies to accounts opened after October 3, 2017 when the “covered borrowers” provision was put into effect.

Who it protects: A “covered borrower” is defined as active duty service members and their dependents (enrolled in deers).

What it does: Protects against predatory lending and caps the Military Annual Percentage Rate (MAPR) at 36% for certain loans and credit cards.

KEY POINT: SCRA & MLA DO NOT REQUIRE FEE WAIVERS

Many people are surprised to learn this… there is no law that requires banks to waive annual fees.

Instead, some banks have chosen to waive fees voluntarily as part of their military support programs and to stay under the 36% MAPR cap. It is a policy decision by these banks as part of their commitment to supporting military families. While not law, it is well-documented and widely honored.

Step 2: Determine if You Qualify

SCRA – credit must be acquired before your orders start on active duty and either:

- Active duty US military on Title 10 orders in the Army, Navy, Air Force, Space Force, Marines, or Coast Guard

- National Guard or Reservists on 30 day or greater active duty orders (such as Title 32, Title 10)

- Public Health Service and NOAA Commissioned Officers

The easiest way to confirm is to check the SCRA Database

MLA – credit must be acquired while you or your sponsor is on active duty orders greater than 30 days and either:

- Active duty member of the Army, Navy, Marines, Air Force, Space Force, or Coast Guard

- Guard or Reservists on 30 day or greater active orders

- A spouse or child dependent of an Active Duty member of the Armed Forces as defined in 38 USC 101(4)

The easiest way to confirm is to check the SCRA Database

Spouses ARE included in Annual Fee Waiver Under MLA

Banks specifically state that qualifying dependents are eligible for the same benefits as the service member under MLA. This isn’t a “loophole” or “cheating the system”. It’s exactly how the banks designed their programs. Military families face unique challenges, and these benefits are meant to support the entire household.

As a reminder, in order to apply MLA benefits, the credit MUST be established AFTER the service member is on active orders greater than 30 days. Annual fees are NOT waived for spouses under SCRA.

Step 3: Know the Banks That Waive Annual Fees

Here’s a breakdown of which banks waive annual fees and under which program. This is where most people get confused — so keep this handy:

Banks That Waive Fees Under MLA (Active Duty + Dependents)

American Express – waives annual fees on all personal cards

Chase – waives annual fees on all personal cards

Citi – waives annual fees on all personal cards

U.S. Bank – waives annual fees on all personal cards

Bank of America – waives annual fees on personal cards over $100 (newer data point)

Banks That Waive Fees Under SCRA (Pre-Service Accounts) Service member only

American Express- waives annual fees to the service member only if opened before entering active duty.

Capital One – waives annual fees to the service member only if the account was opened before entering active duty.

Complete Card Lists by Bank

Want to know exactly which cards get waived? Here’s the full breakdown.

AMERICAN EXPRESS:

- The Platinum Card® from American Express

- American Express® Gold Card

- American Express® Green card

- Blue Cash Preferred® Card from American Express

- Blue Cash Everyday® Card from American Express

- Delta SkyMiles® Gold American Express Card

- Delta SkyMiles® Platinum American Express Card

- Delta SkyMiles® Reserve American Express Card

- Marriott Bonvoy Brilliant® American Express® Card

- Hilton Honors American Express Surpass Card

- Hilton Honors American Express Aspire Card

CHASE:

- Chase Sapphire Reserve®

- Chase Sapphire Preferred®

- Southwest Rapid Rewards® Priority Credit Card

- Southwest Rapid Rewards® Plus Credit Card

- Southwest Rapid Rewards® Premier Credit Card

- Marriott Bonvoy Boundless® Credit Card

- Chase World of Hyatt Credit Card

- IHG® Rewards Premier Credit Card

- United Club Infinite Card

- United Explorer Card

- British Airways Visa Signature® card

- Aer Lingus Visa Signature® card

- Iberia Visa Signature® card

- Disney® Premier Visa® Card

- Starbucks® Rewards Visa® Card

CITI:

- Citi Strata Premier® Card

- Citi Strata Elite℠ Card

- Citi® / AAdvantage® Platinum Select® World Elite Mastercard®

- Citi® / AAdvantage® Executive World Elite Mastercard®

U.S. BANK:

- U.S. Bank Altitude Reserve

- U.S. Bank Altitude® Connect Visa Signature® Card

- U.S. Bank FlexPerks Gold AMEX Card

BANK OF AMERICA:

(These are the cards with annual fees greater than $100 where our Facebook members have confirmed having their fees waived)

- Atmos Rewards Summit Visa Infinite® Card

- Premium Rewards® Elite Credit Card

Step 4: How To Actually Get The Fees Waived

The process to apply MLA benefits should” be automatic when your information is ran through the MLA database.

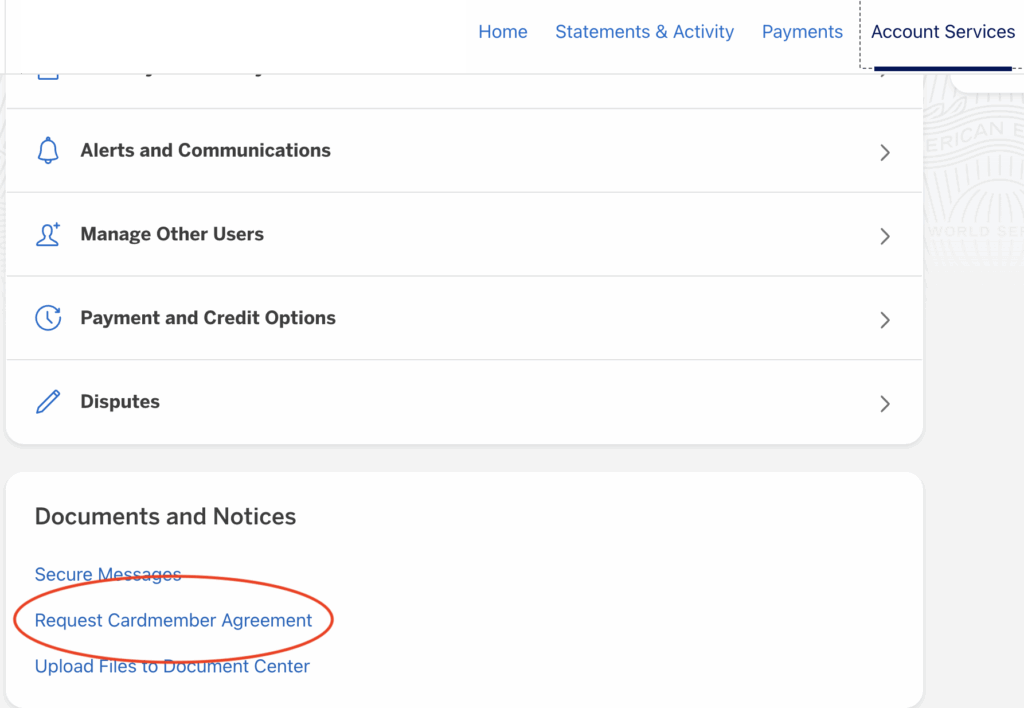

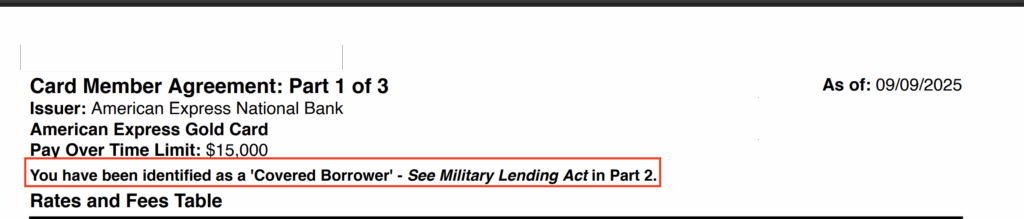

With American Express, you can confirm you have been identified as a “covered borrower” by simply going to the account management page and selecting “request cardmember agreement” at the bottom under “Documents and Notices”

One you open the agreement, you’ll see the following:

With Chase, you’ll receive a MLA fee waiver letter after card approval. Below is a screenshot of a letter one of our team members spouses recently received:

For Citi, if your fees are not waived automatically, we recommend emailing (militaryorders@citi.com) and submitting your MLA eligibility certification from the MLA Database.

Are You a Spouse and Having Issues Getting Your Fee Waived? Here’s a Few Ways to Troubleshoot:

- Make sure your social security number and other information is in DEERS correctly and that you can locate yourself in the database.

- Confirm you are NOT requesting SCRA benefits be applied.

- The annual fee waiver under MLA is only for cards received AFTER Sept 2017 and/or while active duty. If you received a card before then, or before getting married and becoming a spouse to an active duty service member, your fee WILL NOT be waived while that account is open.

Ex: If you received an Amex Gold before Sept 2017 or before becoming a spouse to an AD SM, you would NOT get your fee waived on the Gold card. This fee would not be waived if you tried to upgrade to the Platinum after your service member was active duty either. The only option would be to downgrade your Gold to a no fee card and then apply for a brand new Platinum card.

Myths to Stop Believing

The service member has to apply first.”

Nope. Either spouse can apply first, and MLA benefits will still apply.

“The spouse has to be an authorized user first.”

Nope again. In fact, this can hurt your points strategy — separate accounts are better for maximizing bonuses.

Final Thoughts

Military annual fee waivers are one of the most powerful benefits available for service members and their families. When used strategically, they can save thousands of dollars per year and unlock premium travel perks for free.

The key is understanding the difference between law vs. bank policy, making sure you open new accounts while MLA applies, and troubleshooting if something doesn’t go through automatically.

View comments

+ Leave a comment